Our homes are so much more than the houses we live in. For many, they’ve also become our workplaces, schools for our children, and safe harbors in which we’ve weathered the toughest moments of a global pandemic. Today, 65.6% of Americans call their homes their own, a rate that has risen to its highest point in 8 years.

As National Homeownership Month kicks off this June, homeowners have every reason to celebrate. A survey by Gallup just ranked real estate as the best investment you can make for the eighth year in a row. However, unlike other investment options, the benefits of owning a home aren’t purely financial. Here are the top ways Americans are winning by owning a home.

Non-Financial Benefits:

1. Civic Participation: Owning a home is owning a part of your neighborhood. Homeowners have a stronger connection to their neighborhoods and are more committed to volunteer work and other ways to get involved.

2. Pride of Ownership: Owning a home is having a space that is uniquely yours. You can customize it to your personal liking and make it reflect your personality and values.

3. A Safe Space: Owning a home gives you a sense of security and privacy – two things that have become even more valuable as we’ve tackled the challenges of the recent health crisis.

Financial Benefits:

1. Forced Savings: Owning a home builds equity. Your equity grows with each payment you make toward your mortgage. This form of forced savings can be used down the road to help you accomplish your biggest financial goals.

2. Appreciation: Owning a home is making an investment that steadily gains value, and experts project home values will continue to rise in the years to come.

3. Stability: Owning a home means having better control over your future housing payments. Over the years, a mortgage stays relatively steady, but rent costs continue to rise.

Bottom Line

If you own your home, take time this June to celebrate the ways homeownership has added value to your life. If you hope to become a homeowner this year, let’s connect today to take the first steps toward achieving your goal.

This year, Americans are moving for a variety of reasons. The health crisis has truly reshaped our lifestyles and our needs. Spending so much more time in our current homes has driven many people to reconsider what homeownership means and what they find most valuable in their living spaces.

“For customers who cited COVID-19 as an influence on their move in 2020, the top reasons associated with COVID-19 were concerns for personal and family health and wellbeing (60%); desires to be closer to family (59%); 57% moved due to changes in employment status or work arrangement (including the ability to work remotely); and 53% desired a lifestyle change or improvement of quality of life.”

With a new perspective on homeownership, here are some of the reasons people are reconsidering where they live and making moves right now.

1. Working from Home

Remote work became the new norm, and for some, it’s persisting longer than initially expected. Many in the workforce today are discovering they don’t need to live so close to the office anymore and they can get more for their money if they move a little further outside the city limits. Apartment Listnotes:

“The COVID pandemic has sparked a rebound in residential migration: survey data suggest that 16 percent of American workers moved between April 2020 and April 2021, up from 14 percent in 2019 and the first increase in migration in over a decade… One of the major drivers in this trend is remote work, which expanded greatly in response to COVID and will remain prevalent even after the pandemic wanes. No longer tethered to a physical job site, remote workers were 53 percent more likely to move this past year than on-site workers.”

If you’ve tried to convert your guest room or your dining room into a home office with minimal success, it may be time to find a larger home. The reality is, your current house may not be optimally designed for this kind of space, making remote work very challenging.

2. Room for Fitness & Activities

Staying healthy and active is a top priority for many Americans, and dreams of having space for a home gym are growing stronger. A recent survey of 4,538 active adults from 122 countries noted the three fastest-growing fitness trends amongst active adults:

At-home fitness equipment (up 50%)

Personal trainers/nutritionists (up 48%)

Online fitness courses, classes, and subscriptions (up 17%)

Having room to maintain a healthy lifestyle at home – physically and mentally – may prompt you to consider a new place to live that includes space for at-home workouts, hobbies, and activities for your household.

3. Outdoor Space

Better Homes & Gardens recently released the outdoor living trends for this year, and three of them are:

Outdoor Kitchens: 60% of homeowners are looking to add outdoor kitchens.

Edible Garden: Millions of people began gardening during the pandemic . . . to supplement pantries with homegrown fruits, vegetables, and herbs.

Secluded Spaces: As outdoor activity increases, so does the need for privacy.

You may not, however, currently have the space you need for these designated areas – inside or out.

Bottom Line

If you’re clamoring for more room to accommodate your changing needs, making a move may be your best bet, especially while you can take advantage of today’s low mortgage rates. It’s a great time to get more home for your money, just when you need it most.

There’s a lot of discussion about affordability as home prices continue to appreciate rapidly. Even though the most recent index on affordability from the National Association of Realtors (NAR) shows homes are more affordable today than the historical average, some still have concerns about whether or not it’s truly affordable to buy a home right now.

When addressing this topic, there are various measures of affordability to consider. However, very few of the indexes compare the affordability of owning a home to renting one. In a paper just published by the Urban Institute, Homeownership Is Affordable Housing, author Mike Loftin examines whether it’s more affordable to buy or rent. Here are some of the highlights included.

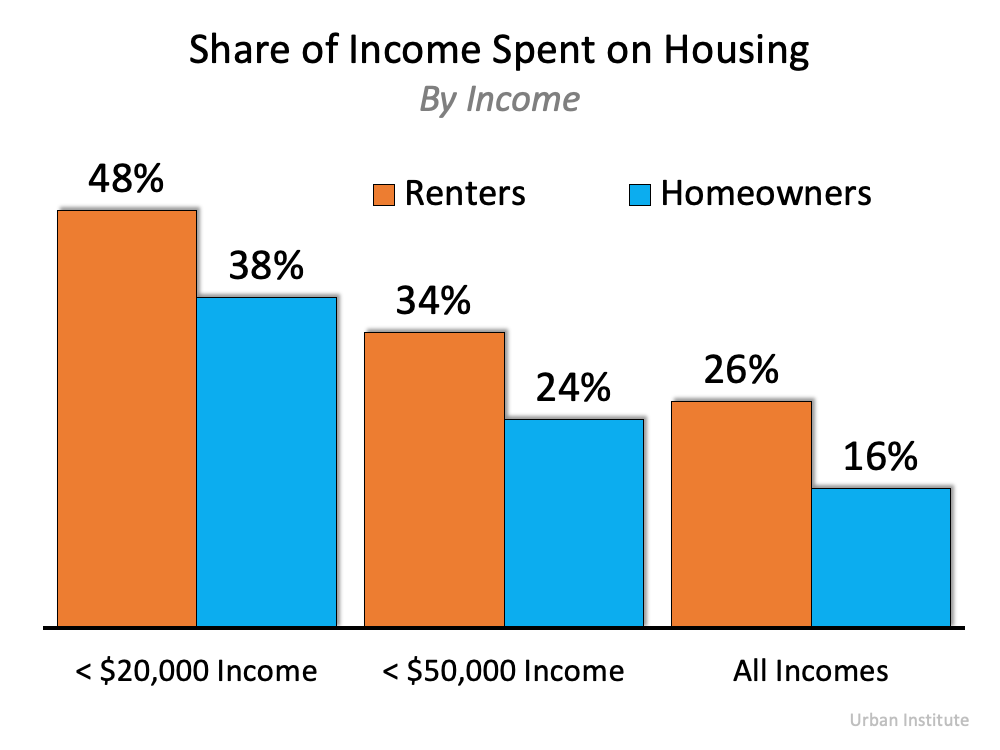

1. Renters pay a higher percentage of their income toward their rental payment than homeowners pay toward their mortgage.

The report explains:

“When we look at the median housing expense ratio of all households, the typical homeowner household spends 16 percent of its income on housing while the typical renter household spends 26 percent. This is true, you might say, because people who own their own home must make more money than people who rent. But if we control for income, it is still more affordable to own a home than to rent housing, on average.”

Here’s the data from the report shown in a graph:

2. Renters don’t have extra money to invest in other assets.

The report goes on to say:

“Buying a home is not a decision between investing in real estate versus investing in stocks, as financial advisers often claim. Instead, the home buying investment simply converts some portion of an existing expense (renting) into an investment in real estate.”

It explains that you still have a housing expense (rent payments) even if you don’t buy a home. You can’t live in your 401K, but you can transfer housing expenses to your real estate investment. A mortgage payment is forced savings; it goes toward building equity you will likely get back when you sell your home. There’s no return on your rent payments.

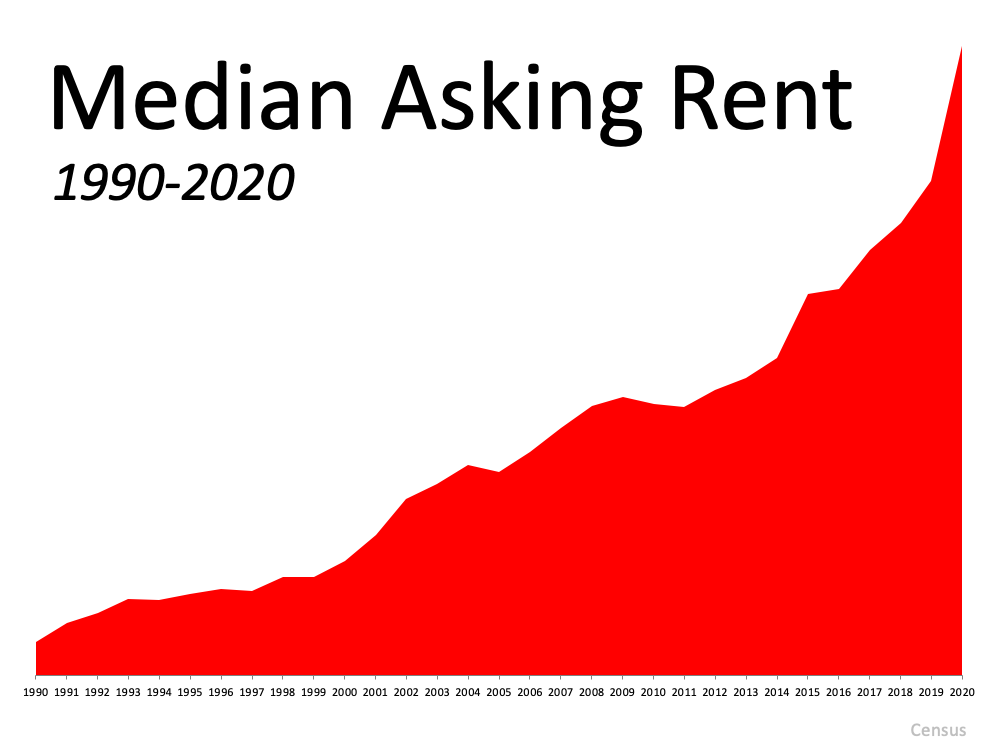

3. Your mortgage payment remains relatively the same over time. Your rent keeps going up.

The report also notes:

“Whereas renters are continuously vulnerable to cost increases, rising home prices do not affect homeowners. Nobody rebuys the same home every year. For the homeowner with a fixed-rate mortgage, monthly payments increase only if property taxes and property insurance costs increase. The principal and interest portion of the payment, the largest portion, is fixed. Meanwhile, the renter’s entire payment is subject to inflation.

Consequently, over time, the homeowner’s and renter’s differing trajectories produce starkly different economic outcomes. Homeownership’s major affordability benefit is that it stabilizes what is likely the homeowner’s biggest monthly expense, assuming a buyer has a fixed-rate mortgage, which most American homeowners do. The only portion of the homeowner’s housing expenses that can increase is taxes and insurance. The principal and interest portion stays the same for 30 years.”

A mortgage payment remains about the same over the 30 years of the mortgage. Here’s what rents have done over the last 30 years:

4. If you want to own a home and can afford it, waiting could cost you.

As the report also indicates:

“We need to stop seeing housing as a reward for financial success and instead see it as a critical tool that can facilitate financial success. Affordable homeownership is not the capstone of economic well-being; it is the cornerstone.”

Homeownership is the first rung on the ladder of financial success for most households, as their home is most often their largest asset.

Bottom Line

If the current headlines reporting a supposed drop-off in home affordability are making you nervous, let’s connect to go over the real insights into our area.

Today’s housing market is full of unprecedented opportunities. High buyer demand paired with record-low housing inventory is creating the ultimate sellers’ market, which means it’s a fantastic time to sell your house. However, that doesn’t mean sellers are guaranteed success no matter what. There are still some key things to know so you can avoid costly mistakes and win big when you make a move.

1. Price Your House Right

When inventory is low, like it is in the current market, it’s common to think buyers will pay whatever we ask when setting a listing price. Believe it or not, that’s not always true. Even in a sellers’ market, listing your house for the right price will maximize the number of buyers that see your house. This creates the best environment for bidding wars, which in turn are more likely to increase the final sale price. A real estate professional is the best person to help you set the best price for your house so you can achieve your financial goals.

2. Keep Your Emotions in Check

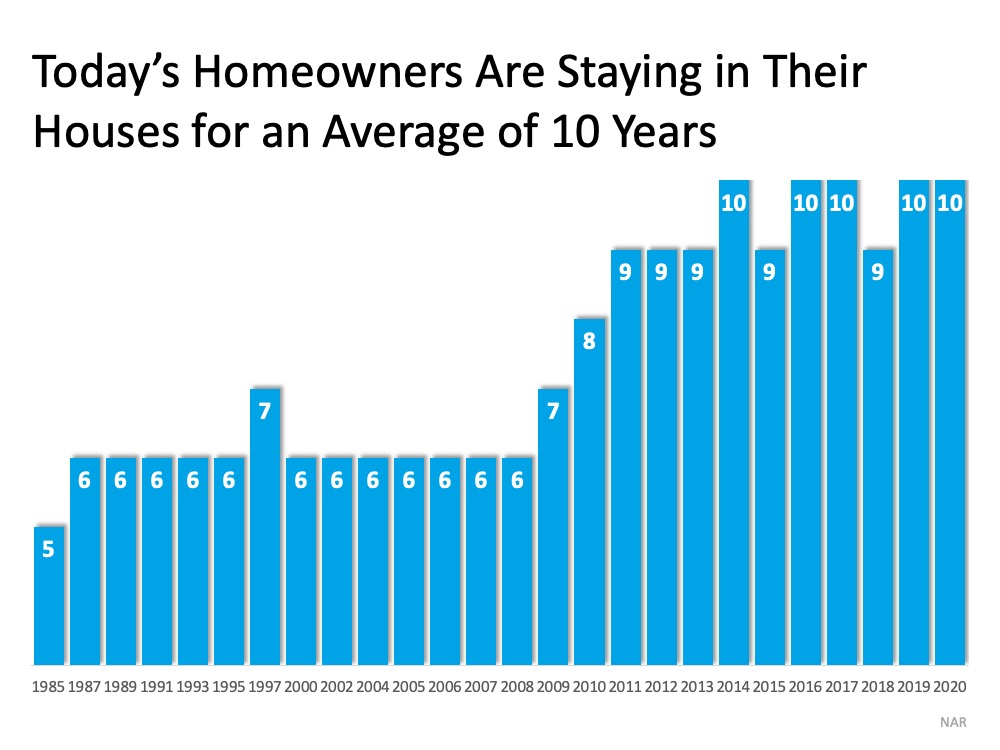

Today, homeowners are living in their houses for a longer period of time. Since 1985, the average time a homeowner owned their home, or their tenure, has increased from 5 to 10 years (See graph below):This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you purchased or the house where your children grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from that sentimental value.

For some homeowners, that connection makes it even harder to separate the emotional value of the house from the fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

3. Stage Your House Properly

We’re generally quite proud of our décor and how we’ve customized our houses to make them our own unique homes. However, not all buyers will feel the same way about your design and personal touches. That’s why it’s so important to make sure you stage your house with the buyer in mind.

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. Stage, clean, and declutter so they can visualize their own dreams as they walk through each room. A real estate professional can help you with tips to get your home ready to stage and sell.

Bottom Line

Today’s sellers’ market might be your best chance to make a move. If you’re considering selling your house, let’s connect today so you have the expert guidance you need to navigate through the process and prioritize these key elements.

The last year has put emphasis on the importance of one’s home. As a result, some renters are making the jump into homeownership while some homeowners are re-evaluating their current house and considering a move to one that better fits their current lifestyle. Understanding how housing affordability works and the main market factors that impact it may help those who are ready to buy a home narrow down the optimal window of time in which to make a purchase.

There are three main factors that go into determining how affordable homes are for buyers:

Mortgage Rates

Mortgage Payments as a Percentage of Income

Home Prices

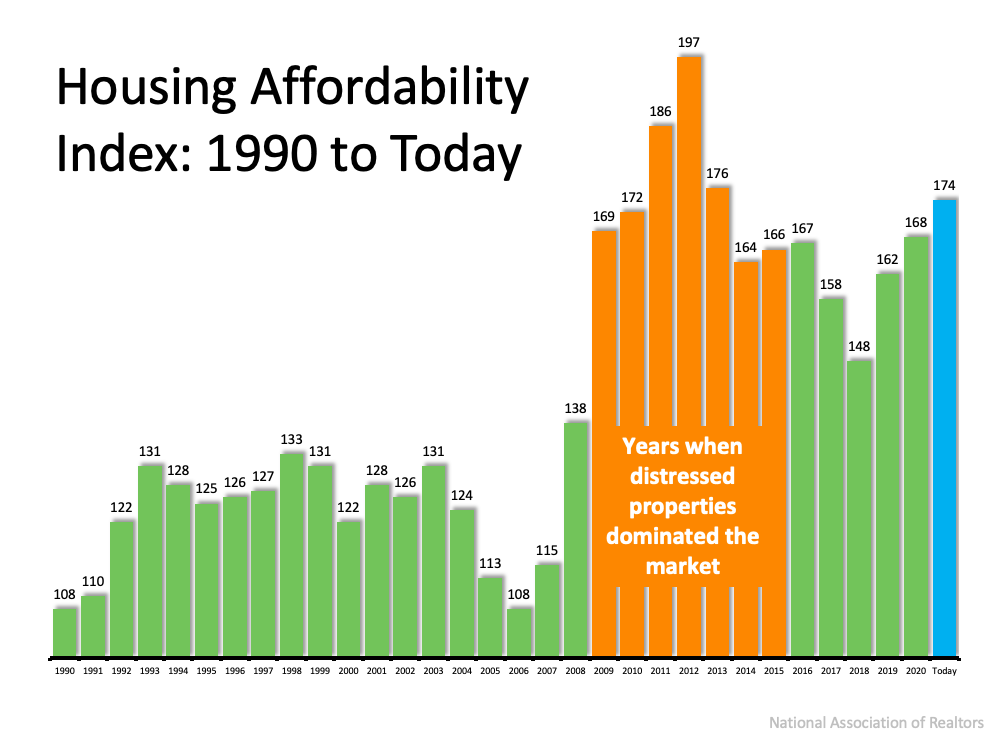

The National Association of Realtors (NAR) produces a Housing Affordability Index. It takes these three factors into account and determines an overall affordability score for housing. According to NAR, the index:

“…measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.”

Their methodology states:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home. An index above 100 signifies that family earning the median income has more than enough income to qualify for a mortgage loan on a median-priced home, assuming a 20 percent down payment.”

So, the higher the index, the more affordable it is to purchase a home. Here’s a graph of the index going back to 1990:The blue bar represents today’s affordability. We can see that homes are more affordable now than they’ve been at any point since the housing crash when distressed properties (foreclosures and short sales) dominated the market. Those properties were sold at large discounts not seen before in the housing market for almost one hundred years.

Why are homes so affordable today?

Although there are three factors that drive the overall equation, the one that’s playing the largest part in today’s homebuying affordability is historically low mortgage rates. Based on this primary factor, we can see that it’s more affordable to buy a home today than at any time in the last eight years.

If you’re considering purchasing your first home or moving up to the one you’ve always hoped for, it’s important to understand how affordability plays into the overall cost of your home. With that in mind, buying while mortgage rates are as low as they are now may save you quite a bit of money over the life of your home loan.

Bottom Line

If you feel ready to buy, purchasing a home this summer may save you a significant amount of money over time based on historical affordability trends. Let’s connect today to determine if now is the right time for you to make your move.

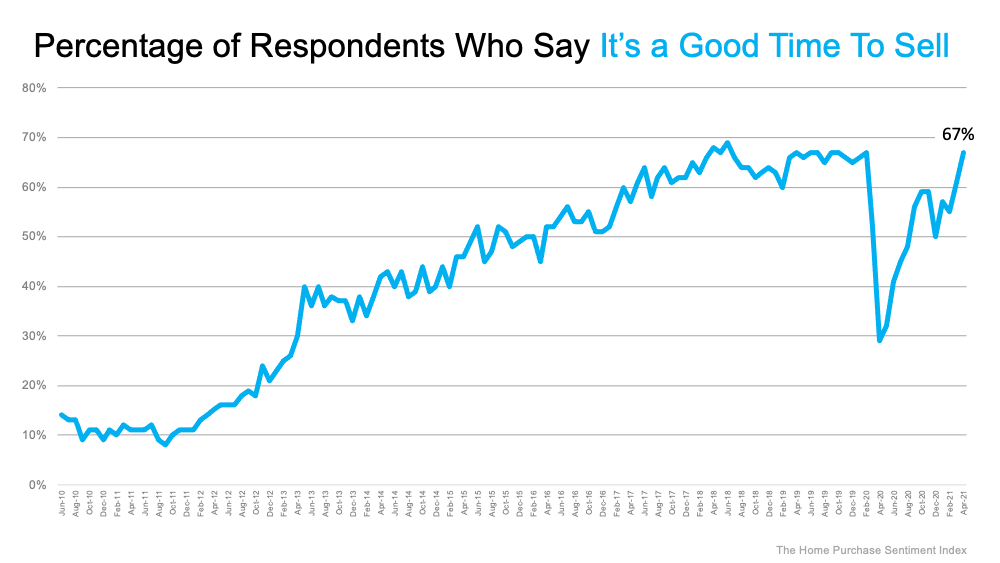

One of the biggest questions in real estate today is, “When will sellers return to the housing market?” An ongoing shortage of home supply has created a hyper-competitive environment for hopeful buyers, leading to the ultimate sellers’ market. However, as the economy continues to improve and more people get vaccinated, more sellers may finally be in sight.

The Home Purchase Sentiment Index (HPSI) by Fannie Mae recently noted the percentage of consumer respondents who say it’s a good time to sell a home increased from 61% to 67%. Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae, indicates:

“Consumer positivity regarding home-selling conditions nearly matched its all-time high.” (See graph below):

Fannie Mae isn’t the only expert group noticing a rise in the percentage of people thinking about selling. George Ratiu, Senior Economist at realtor.com, shares:

“The results of a realtor.com survey . . . showed that one-in-ten homeowners plans to sell this year, with 63 percent of those, looking to list in the next 6 months. Just as encouragingly, close to two-thirds of sellers plan to sell their homes at prices under $350,000, which would offer a tremendous boost to affordable housing for first-time buyers.”

The level of equity homeowners have is at an all-time high. According to the U.S. Census, over 38% of owner-occupied homes are owned free and clear, meaning they don’t have a mortgage. Those with a mortgage are seeing their equity skyrocket too. Every time real estate values increase, homeowners get a dollar-for-dollar gain in their home equity.

“17.8 million residential properties in the United States were considered equity-rich, meaning that the combined estimated amount of loans secured by those properties was 50 percent or less of their estimated market value.

The count of equity-rich properties in the first quarter of 2021 represented 31.9 percent, or about one in three, of the 55.8 million mortgaged homes in the United States. That was up from 30.2 percent in the fourth quarter of 2020, 28.3 percent in the third quarter and 26.5 percent in the first quarter of 2020.”

This surge in home equity has given most homeowners the opportunity to use that equity in one of two ways:

Refinance to cash out some of the equity or lower their current payment

Move to a home that better fits their current needs

Let’s break down the possibilities.

1. Refinance

An abundance of equity and record-low mortgage rates can make refinancing a home very easy. Some homeowners choose to refinance so they can lower their payments. Others convert a portion of the equity to cash while keeping their monthly payment the same.

There are many homeowners who could take advantage of lower rates and higher levels of equity, but they haven’t yet. According to an Economic & Housing Research Note from earlier this month, there were over five million homeowners with a loan funded by Freddie Mac who would benefit by refinancing their loan. As of January 2021, there were:

452,122 loans with an average mortgage rate of 6.17%

1,027,834 loans with an average mortgage rate of 4.39%

3,687,780 loans with an average mortgage rate of 4.21%

With mortgage rates currently hovering around 3%, any of these homeowners would benefit from refinancing. They could lower their payments by hundreds of dollars per month or cash out large sums of equity while keeping their monthly payment the same.

Example:

If a homeowner has a $200,000 fixed-rate mortgage with a 6% interest rate and refinances that loan to a 3% interest rate, their monthly mortgage payment (principal and interest) will go from $1,199 per month to $843 per month – a savings of $356 a month, or $4,272 each year.

On the other hand, if they keep their mortgage payment the same, they could cash out a significant amount of their equity.

2. Move into your dream home

The past year prompted many households to redefine what a dream home really means, and it’s something different to everyone. Those who have a high mortgage rate could use their equity as a down payment and perhaps buy their next home without significantly raising their mortgage payment.

Example:

Suppose a person bought a house for $216,000 at the height of the market in 2006. (The median home price in May of 2006). If they put 10% down and took out a mortgage of $194,400 at 6.41% (the average rate in 2006), the monthly mortgage payment (principal and interest) would have been $1,217.

According to the National Association of Realtors (NAR), a typical single-family home has grown in value by approximately $150,000 over the last fifteen years. That means the $216,000 house would be worth about $366,000 today.

After deducting selling expenses, they would be left with about $130,000 ($150,000 minus approximately $20,000 in selling expenses).

A seller could take that equity and use it as a down payment on a new house. Let’s assume they purchased a home for $450,000 (roughly $80,000 more than the value of their current home). If they put the $130,000 down, they could take out a mortgage of $320,000 with a 3% interest rate. The monthly mortgage payment (principal and interest) would be $1,349. Therefore, they could buy a home worth $80,000 more than the one they have today and only spend an extra $132 per month.

Bottom Line

Whether you’re refinancing your house or moving to a new home, your current mortgage rate and your level of equity are crucial in your decision-making process. Look at your mortgage documentation to find out your interest rate, and then let’s connect to determine the potential equity in your home. You may be surprised by the opportunities you have.

Many people are sitting on the fence trying to decide if now’s the time to buy a home. Some are renters who have a strong desire to become homeowners but are unsure if buying right now makes sense. Others may be homeowners who are realizing that their current home no longer fits their changing needs.

To determine if they should buy now or wait another year, they both need to ask two simple questions:

Do I think home values will be higher a year from now?

Do I think mortgage rates will be higher a year from now?

Let’s shed some light on the answers to these questions.

Where will home prices be a year from now?

If you average the most recent projections from the major industry forecasters, the expectation is home prices will increase by 7.7%. Let’s take a house that’s valued today at $325,000 as an example.

If the buyer makes a 10% down payment ($32,500), they’ll end up borrowing $292,500 for their mortgage. Applying the projected rate of home price appreciation, that same house will cost $350,025 next year. With a 10% down payment ($35,003), they’d then have to borrow $315,022.

Therefore, as a result of rising home prices alone, a prospective buyer will have to put down an additional $2,503 and borrow an additional $22,523 just for waiting a year to make their move.

Where will mortgage rates be a year from now?

Today, mortgage rates are hovering around 3%. However, most experts believe they’ll rise as the economy continues to recover. Any increase in the mortgage rate will also increase a purchaser’s cost. Here are the forecasts for the first quarter of 2022 from four major entities:

The projections average out to 3.6% among these four forecasts, a jump up from where they are today.

What does it mean to you if home values and mortgage rates increase?

A buyer will pay a lot more in mortgage payments each month if both of these variables increase. Assuming a buyer purchases a $325,000 home this year with a 30-year fixed-rate loan at 3% after making a 10% down payment, their monthly principal and interest payment would be $1,233.

That same home one year from now could be $350,025, and the mortgage rate could be 3.6% (based on the industry forecasts mentioned above). That monthly principal and interest payment, after putting down 10%, totals $1,432.

The difference in the monthly mortgage payment would be $199. That’s $2,388 more per year and $71,640 over the life of the loan.

Add to that the approximately $25,000 a house with a similar value would build in home equity this year as a result of home price appreciation, and the total net worth increase a purchaser could gain by buying this year is nearly $100,000. That’s a small fortune.

Bottom Line

When asking if they should buy a home, many potential buyers think of the nonfinancial benefits of owning a home. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

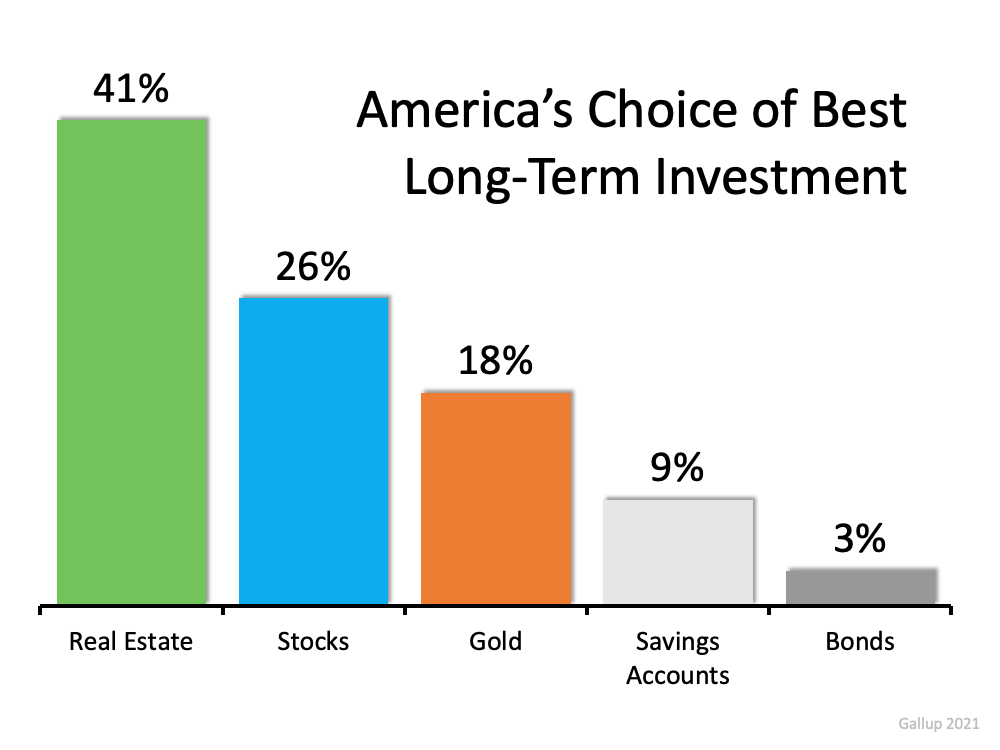

Last month, in a post on the Liberty Street Economics blog, the Federal Reserve Bank of New York noted that Americans believe buying a home is definitely or probably a better investment than buying stocks. Last week, a Gallup Poll reaffirmed those findings.

In an article on the current real estate market, Gallup reports:

“Gallup usually finds that Americans regard real estate as the best long-term investment among several options — seeing it as superior to stocks, gold, savings accounts and bonds. This year, 41% choose real estate as the best investment, up from 35% a year ago, with stocks a distant second.”

Here’s the breakdown:The article goes on to say:

“The 41% choosing real estate is the highest selecting any of the five investment options in the 11 years Gallup has asked this question.”

Is real estate really a secure investment right now?

Some question American confidence in real estate as a good long-term investment right now. They fear that the build-up in home values may be mirroring what happened right before the housing crash a little more than a decade ago. However, according to Merrill Lynch, J.P. Morgan, Morgan Stanley, and Goldman Sachs, the current real estate market is strong and sustainable.

As Morgan Stanley explains to their clients in a recent Thoughts on the Marketpodcast:

“Unlike 15 years ago, the euphoria in today’s home prices comes down to the simple logic of supply and demand. And we at Morgan Stanley conclude that this time the sector is on a sustainably, sturdy foundation . . . . This robust demand and highly challenged supply, along with tight mortgage lending standards, may continue to bode well for home prices. Higher interest rates and post pandemic moves could likely slow the pace of appreciation, but the upward trajectory remains very much on course.”

Bottom Line

America’s belief in the long-term investment value of homeownership has been, is, and will always be, very strong.

Homebuyers make up their minds about a property in the first few minutes. Make sure your home makes that vital first impression. New paint does wonders. Make sure the front yard is flawless with manicured lawns and attractive foliage. Add a hanging basket or some flower pots at the door. The front door is also critical, make sure the hardware is presentable.

Make them Feel Welcome

Don’t forget buying a home is in many ways an emotional decision, so it’s important to give buyers that warm and fuzzy feeling! Keep the temperature in the home at a comfortable level. Light some candles in the bathrooms and make sure it smells nice and clean. Have fresh flowers around the house.

But don’t make it too personal

Make them feel welcome, but don’t go too far. Too much personality, for example in the form of personal possessions and family photos makes it hard for buyers to visualize living in the space.

Clear out the Clutter

Make sure your property is clutter-free for all your viewings. This will make your home look and feel bigger, and the buyers will be able to imagine how they could make the space their own. Make sure that there is a clean, logical flow through the home by getting rid of all excess furniture. Less is more.

Improve Lighting

This is another way to make your home seem more spacious. Open all your curtains and flood the space with natural light. Make sure the darker rooms are also lit. Invest in some light fixtures and fittings, and place them strategically to illuminate even the gloomiest of areas.

Decorate to Sell That House

Slap on a fresh coat of paint in a neutral color to give it that blank canvas look but do not be too sterile. Have some contrast in the trim as well as the ceiling. Neutral colors make properties appear lighter and brighter, so take advantage of this inexpensive and easy option. You may also add color with decorative window coverings, rugs, and towels.

Clean Up Your Act

Your home should be spotless. Make sure the beds are made and the countertops are free of clutter. The dishes should be put away and nothing should be scattered on the floor. Don’t forget to tidy your garden too: Cut the shrubs back, sweep the patio, and wipe down the backyard furniture.

Those Minor Repairs You Put Off

It is easy to forget things such as broken doorknobs, cracked tiles, holes in walls and damaged but buyers will notice them first thing as they are walking around your home.

Maximize Your Space

The golden rule of selling is to make your space look and feel bigger and better than what your competitors have to offer. We’ve already mentioned that lighting your home, both naturally and artificially, can maximize your assets, but getting rid of bulky furniture can also be a great way of making the most of what you have. Large pieces of furniture make a space feel smaller, so put these items into storage and dress your home with more compact pieces.

Don’t Forget Your Floors

Make the investment of improving and investing in those floors. Worn carpets and damaged vinyl floors need to be replaced, and wooden floors especially should undergo some maintenance. This is not chap by any means, but the prospect of selling your home for the best possible price will likely outweigh the cost.

Remove Pets During Showings

You do not need to remind the potential buyer that the previous owner kept pets.

Try to remove your pets from your home when you are showing the home. Having a pet in the house or yard can create complications for your agent while trying to show the house, and puts your pet at risk of accidentally getting out during the showing. There are also liability issues to deal with as well. They may react differently to stranger and it may cause them stress. All pet-related damage should be repaired prior to showing the home. Make sure to also remove all odors and stains. New visitors will notice smells when they come to view the house. This is not something you want to happen. Have your carpet and floors professionally cleaned or replaced. Pick up any messes in the backyard and have any sod replaced and other damage repaired.